According to Herzberg's Two-Factor Theory of Motivation, which of the following is a factor mentioned most often by satisfied employees?

Security.

Status.

Recognition.

Relationship with coworkers

Herzberg's Two-Factor Theory of Motivation divides workplace factors into:

Hygiene factors (which prevent dissatisfaction but do not increase satisfaction) – e.g., salary, security, relationships.

Motivators (which drive job satisfaction and performance) – e.g., recognition, achievement, responsibility, and personal growth.

Employees most often mention recognition as a key factor in job satisfaction, as it directly impacts motivation and engagement.

(A) Incorrect – Security.

Job security is a hygiene factor, meaning its absence causes dissatisfaction, but its presence does not create job satisfaction.

(B) Incorrect – Status.

Status is a hygiene factor, not a motivator. It prevents dissatisfaction but does not enhance motivation significantly.

(C) Correct – Recognition.

Recognition is a motivator, meaning it actively increases job satisfaction and is frequently cited by happy employees.

(D) Incorrect – Relationship with coworkers.

Work relationships are hygiene factors. While poor relationships can lead to dissatisfaction, strong relationships alone do not create motivation.

IIA’s Global Internal Audit Standards – Human Resources and Organizational Behavior

Discusses motivation theories and their impact on employee performance.

Herzberg’s Two-Factor Theory of Motivation

Identifies recognition as a primary factor for employee satisfaction.

Analysis of Answer Choices:IIA References and Internal Auditing Standards:

Which of the following activities best illustrates a user's authentication control?

Identity requests are approved in two steps.

Logs are checked for misaligned identities and access rights.

Users have to validate their identity with a smart card.

Functions can toe performed based on access rights

Authentication control is a security measure used to verify the identity of users before granting access to systems or data. Authentication methods ensure that only authorized individuals can access resources.

Why Option C (Users have to validate their identity with a smart card) is Correct:

Authentication is the process of verifying a user’s identity before granting access.

Smart card authentication is a strong authentication method because it requires a physical device (smart card) and a PIN or biometric verification.

This falls under multi-factor authentication (MFA), enhancing security by combining something the user has (smart card) with something they know (PIN).

Why Other Options Are Incorrect:

Option A (Identity requests are approved in two steps):

Incorrect because this refers to identity approval (authorization), not authentication.

Option B (Logs are checked for misaligned identities and access rights):

Incorrect because log monitoring is a detective control, not an authentication control.

Option D (Functions can be performed based on access rights):

Incorrect because this describes authorization (determining what a user can do after authentication).

IIA GTAG – "Auditing Identity and Access Management": Covers authentication methods like smart cards and multi-factor authentication.

COBIT 2019 – DSS05 (Manage Security Services): Recommends strong authentication controls, including smart card validation.

NIST Cybersecurity Framework – "Access Control Guidelines": Highlights authentication best practices, including smart card use.

IIA References:

When determining the level of physical controls required for a workstation, which of the following factors should be considered?

Ease of use.

Value to the business.

Intrusion prevention.

Ergonomic model.

When determining the level of physical controls required for a workstation, the most critical factor is its value to the business. Physical controls are security measures implemented to protect assets from unauthorized access, damage, or theft.

Asset Value → Determines the level of protection required.

Risk Assessment → Identifies threats like theft, sabotage, or natural disasters.

Compliance Requirements → Ensures alignment with security regulations and best practices.

(A) Ease of use.

Incorrect: While user-friendliness is important, security measures are primarily based on asset value and risk, not convenience.

IIA Standard 2110 (Governance) emphasizes security over ease of use.

(B) Value to the business. (Correct Answer)

The higher the workstation's importance to business operations, the stronger the physical controls required.

Workstations handling sensitive data or critical systems require additional security.

COSO ERM – Risk Assessment requires evaluating asset value when designing security controls.

(C) Intrusion prevention.

Partially correct but secondary: Intrusion prevention is one of many security concerns, but the primary driver for determining physical controls is the asset’s business value.

(D) Ergonomic model.

Incorrect: Ergonomics is about user comfort and efficiency, not security.

IIA Standard 2120 – Risk Management: Requires risk-based decision-making, including evaluating asset value.

GTAG 9 – Identity and Access Management: Stresses that security measures must align with asset value and business risk.

COSO ERM – Risk Assessment: Establishes asset value as a key determinant in risk-based security controls.

Factors Considered in Physical Security Decisions:Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (B) because the level of physical controls should be determined based on how critical the workstation is to business operations.

An organization decided to reorganize into a flatter structure. Which of the following changes would be expected with this new structure?

Lower costs.

Slower decision making at the senior executive level.

Limited creative freedom in lower-level managers.

Senior-level executives more focused on short-term, routine decision making

A flatter organizational structure reduces hierarchical levels and promotes greater autonomy for employees. The primary benefit is cost reduction due to fewer management layers and streamlined decision-making.

Fewer Management Layers – Reduces the number of mid-level managers, decreasing salary expenses.

Increased Operational Efficiency – Less bureaucracy leads to faster decision-making, lowering administrative costs.

Encourages Employee Autonomy – Reduces dependence on supervision, improving productivity.

B. Slower decision-making at the senior executive level – Incorrect because flatter structures lead to faster decision-making due to fewer approval levels.

C. Limited creative freedom in lower-level managers – Incorrect because flatter structures provide more autonomy and innovation opportunities.

D. Senior-level executives more focused on short-term, routine decision-making – Incorrect because executives in a flatter structure focus on strategic, high-level decisions, delegating routine tasks.

IIA’s GTAG on Governance and Risk Management – Discusses the financial and operational impacts of different organizational structures.

COSO’s Enterprise Risk Management (ERM) Framework – Emphasizes how flatter structures reduce operational inefficiencies and costs.

COBIT 2019 (Governance Framework) – Highlights the impact of organizational structure on financial performance.

Why Lower Costs is the Correct Answer?Why Not the Other Options?IIA References:

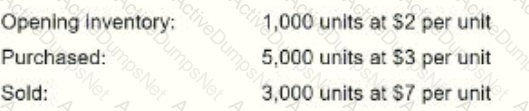

Which of the following represents an inventory costing technique that can be manipulated by management to boost net income by selling units purchased at a low cost?

First-in. first-out method (FIFO).

Last-in, first-out method (LIFO).

Specific identification method.

Average-cost method

The FIFO (First-In, First-Out) method values inventory based on the assumption that older, lower-cost inventory is sold first, leaving newer, higher-cost inventory in stock. During periods of rising prices, FIFO results in lower cost of goods sold (COGS) and higher net income, making it susceptible to manipulation by management.

(A) Correct – First-in, first-out method (FIFO).

FIFO lowers COGS when older, cheaper inventory is sold first, inflating net income.

Management can manipulate earnings by selectively selling older, lower-cost inventory.

(B) Incorrect – Last-in, first-out method (LIFO).

LIFO assumes newer, higher-cost inventory is sold first, resulting in higher COGS and lower net income.

LIFO is typically used to reduce taxable income, not to inflate net income.

(C) Incorrect – Specific identification method.

This method tracks the exact cost of each unit, eliminating the ability to manipulate costs easily.

(D) Incorrect – Average-cost method.

The average-cost method smooths out fluctuations in inventory costs, preventing significant income manipulation.

IIA’s Global Internal Audit Standards – Financial Reporting and Inventory Valuation Risks

Discusses inventory accounting methods and their impact on financial statements.

IFRS and GAAP Accounting Standards – Inventory Valuation

Defines how FIFO can be used to influence financial performance.

COSO’s ERM Framework – Financial Manipulation Risks

Identifies inventory valuation as an area where earnings management can occur.

Analysis of Answer Choices:IIA References and Internal Auditing Standards:

A company records income from an investment in common stock when it does which of the following?

Purchases bonds.

Receives interest.

Receives dividends

Sells bonds.

When a company invests in common stock, it can earn income in two primary ways:

Dividend income: When the company receives dividends, it recognizes the income.

Capital gains: When the stock is sold for a higher price than its purchase price, it results in a gain.

Why Option C (Receives dividends) is Correct:

Dividends represent income from an investment in common stock when declared and paid by the issuing company.

Under GAAP and IFRS, dividend income is recognized when received, not when declared.

Companies record dividends as investment income in their income statement.

Why Other Options Are Incorrect:

Option A (Purchases bonds):

Incorrect because purchasing bonds is an investment transaction, not income recognition.

Option B (Receives interest):

Incorrect because interest income applies to bond investments, loans, or deposits, not common stock investments.

Option D (Sells bonds):

Incorrect because selling bonds results in capital gains or losses, not regular investment income from common stock.

IIA Practice Guide – "Auditing Investment & Treasury Activities": Discusses the recognition of investment income.

IFRS 9 (Financial Instruments) & GAAP Standards: Provide guidance on recording dividends as investment income.

COSO Internal Control – Integrated Framework: Emphasizes proper financial reporting and income recognition.

IIA References:

Which of the following inventory costing methods requires the organization to account for the actual cost paid for the unit being sold?

Last-in-first-Out (LIFO}.

Average cost.

First-in-first-out (FIFO).

Specific identification

The specific identification method is an inventory costing approach where the actual cost of each individual unit sold is recorded. This method is used when items are uniquely identifiable, such as in industries dealing with luxury goods, automobiles, or custom-manufactured products.

Correct Answer (D - Specific identification)

Under the specific identification method, each inventory unit is tracked separately, and its actual purchase cost is assigned to the cost of goods sold (COGS) when sold.

This method is commonly used for high-value, low-volume items where unique tracking is feasible.

The IIA’s GTAG 8: Audit of Inventory Management explains how different costing methods impact financial reporting and internal controls.

Why Other Options Are Incorrect:

Option A (LIFO - Last-in, First-out):

LIFO assumes that the most recent (last-in) inventory is sold first, but it does not track actual unit cost. Instead, it assigns the cost of the newest inventory to COGS.

LIFO is often used for tax benefits but does not follow actual unit cost identification.

Option B (Average cost):

The weighted average cost method calculates an average cost for all inventory units rather than assigning actual unit costs.

This method smooths out price fluctuations but does not track specific items' costs.

Option C (FIFO - First-in, First-out):

FIFO assumes that the oldest (first-in) inventory is sold first, assigning its cost to COGS.

However, like LIFO, it does not track individual unit costs.

IIA GTAG 8: Audit of Inventory Management – Explains different inventory costing methods, including specific identification.

IIA Practice Guide: Assessing Inventory Risks – Covers inventory valuation and fraud risks.

Step-by-Step Explanation:IIA References for Validation:Thus, the specific identification method (D) is the only one that accounts for the actual cost paid for each unit sold.

Which of the following best explains the matching principle?

Revenues should be recognized when earned.

Revenue recognition is matched with cash.

Expense recognition is tied to revenue recognition.

Expenses are recognized at each accounting period.

The matching principle is a fundamental accounting concept that ensures that expenses are recorded in the same period as the revenues they help generate.

Why Option C (Expense recognition is tied to revenue recognition) is Correct:

The matching principle states that expenses should be recognized in the same period as the revenue they help generate to ensure accurate financial reporting.

This principle is applied in accrual accounting under GAAP and IFRS, ensuring that expenses and revenues are properly aligned.

Why Other Options Are Incorrect:

Option A (Revenues should be recognized when earned):

This describes the revenue recognition principle, not the matching principle.

Option B (Revenue recognition is matched with cash):

Incorrect because the matching principle applies to accrual accounting, not cash accounting. Revenue can be recognized before cash is received.

Option D (Expenses are recognized at each accounting period):

Incorrect because expenses are not necessarily recognized in every period; they are matched to revenue.

IIA Practice Guide – "Auditing Financial Reporting Controls": Discusses the importance of the matching principle.

GAAP & IFRS Accounting Standards: Define and require the application of the matching principle.

COSO Internal Control Framework: Emphasizes revenue-expense alignment for accurate financial reporting.

IIA References:

Which of the following represents a basis for consolidation under the International Financial Reporting Standards?

Variable entity approach.

Control ownership.

Risk and reward.

Voting interest.

Under International Financial Reporting Standards (IFRS 10 – Consolidated Financial Statements), an entity is required to consolidate its financial statements based on the control principle rather than ownership percentage alone.

Why Option B (Control ownership) is Correct:

According to IFRS 10, consolidation is required when an entity has control over another entity.

Control is defined as having power over the investee, exposure to variable returns, and the ability to influence those returns.

Even if an entity owns less than 50% of voting rights, it may still have control through contractual arrangements, rights over key decisions, or majority board influence.

Why Other Options Are Incorrect:

Option A (Variable entity approach):

This is a concept used in U.S. GAAP (ASC 810 – Variable Interest Entities) rather than IFRS. IFRS focuses on the broader control model.

Option C (Risk and reward):

IFRS previously considered risk and reward under IAS 27/SIC-12, but IFRS 10 replaced this with the control model.

Option D (Voting interest):

Voting rights alone do not determine consolidation under IFRS. Control can exist even without majority voting rights through contractual arrangements or potential voting rights.

IFRS 10 – Consolidated Financial Statements: Defines the principle of control for consolidation.

IIA GTAG – "Auditing Financial Reporting Risks": Discusses the impact of IFRS consolidation principles.

COSO ERM Framework: Emphasizes risk assessment in financial reporting, including consolidation decisions.

IIA References:Thus, the correct answer is B. Control ownership.

Which of the following lists best describes the classification of manufacturing costs?

Direct materials, indirect materials, raw materials.

Overhead costs, direct labor, direct materials.

Direct materials, direct labor, depreciation on factory buildings.

Raw materials, factory employees' wages, production selling expenses.

Manufacturing costs are classified into three main categories: direct materials, direct labor, and manufacturing overhead. These categories help organizations determine product costs, pricing strategies, and financial reporting.

Why Option B (Overhead costs, direct labor, direct materials) is Correct:

Direct materials: Raw materials used directly in production (e.g., wood for furniture).

Direct labor: Labor costs directly tied to production (e.g., factory workers assembling a product).

Manufacturing overhead: Indirect costs related to production (e.g., depreciation, factory utilities, maintenance).

These categories align with GAAP, IFRS, and cost accounting standards.

Why Other Options Are Incorrect:

Option A (Direct materials, indirect materials, raw materials):

"Indirect materials" and "raw materials" are part of manufacturing overhead and direct materials, respectively, but do not form a primary cost classification.

Option C (Direct materials, direct labor, depreciation on factory buildings):

Depreciation on factory buildings is an overhead cost, not a separate category.

Option D (Raw materials, factory employees' wages, production selling expenses):

Selling expenses are not part of manufacturing costs; they are part of operating expenses.

IIA Practice Guide – Auditing Cost Management: Defines manufacturing cost classifications.

IFRS & GAAP Cost Accounting Standards: Outline manufacturing cost components.

COSO Framework – Cost Control Guidelines: Emphasizes accurate cost allocation in financial reporting.

IIA References:

Employees at an events organization use a particular technique to solve problems and improve processes. The technique consists of five steps: define, measure, analyze,

improve, and control. Which of the following best describes this approach?

Six Sigma,

Quality circle.

Value chain analysis.

Theory of constraints.

The Define, Measure, Analyze, Improve, and Control (DMAIC) methodology is the core framework of Six Sigma, a data-driven process improvement approach that aims to reduce defects, enhance efficiency, and optimize performance.

(A) Correct – Six Sigma.

DMAIC is a structured Six Sigma methodology used for problem-solving and process improvement.

It helps organizations identify inefficiencies, eliminate errors, and standardize processes.

(B) Incorrect – Quality circle.

A quality circle is a group of employees who meet to discuss and resolve work-related issues, but it does not follow the structured DMAIC approach.

(C) Incorrect – Value chain analysis.

Value chain analysis focuses on evaluating business activities to improve competitive advantage, not structured process improvement like Six Sigma.

(D) Incorrect – Theory of constraints.

The Theory of Constraints (TOC) focuses on identifying and eliminating bottlenecks in processes, but it does not use the DMAIC approach.

IIA’s Global Internal Audit Standards – Process Improvement and Risk Management

Emphasizes methodologies like Six Sigma for operational efficiency.

COSO’s ERM Framework – Continuous Improvement and Quality Management

Discusses the role of Six Sigma in improving processes and reducing risks.

IIA’s Guide on Business Process Auditing

Recommends structured approaches such as Six Sigma for evaluating process efficiency.

Analysis of Answer Choices:IIA References and Internal Auditing Standards:

Which of the following parties is most likely to be responsible for maintaining the infrastructure required to prevent the failure of a real-time backup of a database?

IT database administrator.

IT data center manager.

IT help desk function.

IT network administrator.

Maintaining the infrastructure for a real-time database backup involves ensuring that backups are correctly configured, continuously running, and fail-safe mechanisms are in place to prevent data loss. The most appropriate role for this responsibility is the IT database administrator (DBA) because:

Primary Role of a DBA:

The DBA is responsible for managing database performance, availability, backup strategies, and recovery processes.

Ensures that real-time backups are functioning properly and failure risks are mitigated.

Database Infrastructure & Backup Strategies:

DBAs configure, monitor, and troubleshoot real-time backup solutions such as replication, mirroring, and log shipping.

They work with backup tools like Oracle Data Guard, SQL Server Always On, and MySQL replication.

Disaster Recovery & Data Integrity:

The DBA ensures data consistency and integrity, especially during system failures or cyber incidents.

They set up recovery point objectives (RPO) and recovery time objectives (RTO) for database resilience.

Option B (IT Data Center Manager):

Oversees physical and environmental infrastructure (e.g., servers, cooling, and power systems). Not directly responsible for database backup failure prevention. (Incorrect)

Option C (IT Help Desk Function):

Provides user support and troubleshooting but does not manage backup infrastructure. (Incorrect)

Option D (IT Network Administrator):

Manages network configurations, security, and connectivity but does not handle database backup infrastructure. (Incorrect)

IIA GTAG – "Auditing Business Continuity and Disaster Recovery": Emphasizes the role of DBAs in backup infrastructure.

COBIT 2019 – BAI10.02 (Manage Backup and Restore): Assigns database backup management responsibilities primarily to DBAs.

IIA's "Auditing IT Operations": Recommends that database administration teams ensure backup mechanisms are tested regularly.

Why Other Options Are Incorrect:IIA References:Thus, the correct answer is A. IT database administrator.

Which of the following IT disaster recovery plans includes a remote site dessgnated for recovery with available space for basic services, such as internet and

telecommunications, but does not have servers or infrastructure equipment?

Frozen site

Cold site

Warm site

Hot site

An IT disaster recovery plan (DRP) ensures business continuity by defining backup and recovery sites. These sites differ based on their level of readiness.

Let’s analyze the answer choices:

Option A: Frozen site

Incorrect. "Frozen site" is not a recognized term in IT disaster recovery planning. The three common categories are cold, warm, and hot sites.

Option B: Cold site

Correct.

A cold site is a designated recovery location that provides only basic facilities such as power, space, internet, and telecommunications.

It does not include servers, infrastructure, or pre-installed systems, meaning that it requires significant setup time before becoming operational.

IIA Reference: Business continuity and IT risk management frameworks classify cold sites as a cost-effective but slower disaster recovery option. (IIA GTAG: Business Continuity Management)

Option C: Warm site

Incorrect. A warm site includes some pre-installed hardware and software, allowing faster recovery compared to a cold site.

Option D: Hot site

Incorrect. A hot site is fully operational with real-time data replication, enabling an immediate switchover in case of disaster.

What is the primary risk associated with an organization adopting a decentralized structure?

Inability to adapt.

Greater costs of control function.

Inconsistency in decision making.

Lack of resilience.

A decentralized structure distributes decision-making authority across different business units, divisions, or geographical locations. While decentralization provides flexibility and autonomy, the primary risk is inconsistency in decision-making, as different units may develop their own policies, processes, and priorities that are not aligned with the organization's strategic goals.

(A) Inability to adapt.

Incorrect. Decentralization typically enhances adaptability, as individual units can quickly respond to local market conditions, customer needs, and emerging risks without waiting for corporate approval.

(B) Greater costs of control function.

Partially correct but not the primary risk. While decentralization may increase oversight costs (e.g., more auditors and compliance personnel), the primary issue is lack of uniform decision-making rather than costs alone.

(C) Inconsistency in decision making. ✅

Correct. When decision-making authority is spread across various units, inconsistencies arise in areas such as risk management, compliance, operational procedures, and resource allocation. This can lead to conflicts, inefficiencies, and misalignment with corporate strategy.

IIA Standard 2120 – Risk Management emphasizes the need for consistent risk oversight in all business units.

IIA GTAG "Auditing the Control Environment" warns that inconsistent policies weaken internal controls and governance.

(D) Lack of resilience.

Incorrect. A decentralized structure often improves resilience because decision-making is spread out, reducing dependency on a central authority. This allows units to function independently if one area experiences disruption.

IIA Standard 2120 – Risk Management

IIA GTAG – "Auditing the Control Environment"

COSO Framework – Internal Control Principles

Analysis of Answer Choices:IIA References:Thus, the correct answer is C, as decentralization introduces decision-making inconsistencies, affecting governance and strategic alignment.

Which of the following IT layers would require the organization to maintain communication with a vendor in a tightly controlled and monitored manner?

Applications

Technical infrastructure.

External connections.

IT management

Organizations that rely on third-party vendors for IT services must ensure secure and controlled communication, especially in areas where external connections are involved. External connections typically include:

Cloud services (e.g., SaaS, PaaS, IaaS)

Third-party APIs

Remote access (VPNs, firewalls, network gateways)

IoT devices and external sensors

These connections introduce cybersecurity risks, requiring continuous monitoring, vendor communication, and security controls.

(A) Applications.

Incorrect. While application security is important, it is typically managed internally. Vendor involvement is needed for software patches and updates, but communication is not as tightly monitored.

(B) Technical infrastructure.

Incorrect. This layer includes internal IT components like servers, databases, and networks, which are mostly managed in-house. Vendor involvement is required for hardware/software updates but not to the same extent as external connections.

(C) External connections. ✅

Correct. External connections require tightly controlled communication with vendors to prevent security breaches, unauthorized access, and data leaks.

IIA GTAG "Auditing IT Governance" highlights third-party risk management as a key area for IT audits.

IIA Standard 2110 requires organizations to establish governance structures for vendor and IT security management.

(D) IT management.

Incorrect. IT management focuses on internal oversight of IT policies and compliance, but does not necessarily require tightly controlled vendor communication.

IIA GTAG – "Auditing IT Governance"

IIA GTAG – "Managing Third-Party Risks"

IIA Standard 2110 – Governance

Analysis of Answer Choices:IIA References:

Which of the following contract concepts is typically given in exchange for the execution of a promise?

Lawfulness.

Consideration.

Agreement.

Discharge

Consideration is a fundamental element of a legally binding contract, referring to something of value exchanged between parties. It ensures that each party receives a benefit or suffers a legal detriment in return for the promise made.

Essential for Contract Enforceability – A contract must involve an exchange of value (e.g., money, services, goods, or a promise to act or refrain from acting).

Legal Reciprocity – Both parties must give and receive something of value to make the contract valid.

Distinguishes Contracts from Gifts – A gift is voluntary and does not require consideration, whereas a contract does.

A. Lawfulness – A contract must be lawful, but lawfulness is a requirement, not something exchanged.

C. Agreement – An agreement is part of a contract, but without consideration, an agreement is not legally binding.

D. Discharge – Discharge refers to ending a contract, not forming one.

IIA’s GTAG on Contract Management Risks – Highlights consideration as a key contract principle.

COSO’s Internal Control Framework – Covers contract law fundamentals in risk management.

Common Law and Uniform Commercial Code (UCC) – Define consideration as an essential element of a contract.

Why Consideration is the Correct Answer?Why Not the Other Options?IIA References:

A manufacturer ss deciding whether to sell or process materials further. Which of the following costs would be relevant to this decision?

Incremental processing costs, incremental revenue, and variable manufacturing expenses.

Joint costs, incremental processing costs, and variable manufacturing expenses.

Incremental revenue, joint costs, and incremental processing costs.

Variable manufacturing expenses, incremental revenue, and joint costs

When deciding whether to sell a product as-is or process it further, a manufacturer should consider only relevant costs—those that will change based on the decision.

Why Option A (Incremental processing costs, incremental revenue, and variable manufacturing expenses) is Correct:

Incremental processing costs: These are additional costs required to process the material further, making them directly relevant.

Incremental revenue: The additional revenue that would be generated if the product is processed further is a key factor in decision-making.

Variable manufacturing expenses: These costs change with production levels, making them important in the decision-making process.

Why Other Options Are Incorrect:

Option B (Joint costs, incremental processing costs, and variable manufacturing expenses):

Incorrect because joint costs (costs incurred before the split-off point) are sunk costs and are not relevant in the decision.

Option C (Incremental revenue, joint costs, and incremental processing costs):

Incorrect because, again, joint costs are not relevant to the decision.

Option D (Variable manufacturing expenses, incremental revenue, and joint costs):

Incorrect because joint costs should be ignored in a sell-or-process-further decision.

IIA GTAG – "Auditing Cost Accounting Decisions": Discusses relevant costs in decision-making.

IFRS & GAAP Cost Accounting Standards: Explain cost classification and decision-making.

COSO Internal Control – Integrated Framework: Recommends proper cost allocation methods for financial decisions.

IIA References:

An organization decided to outsource its human resources function. As part of its process migration, the organization is implementing controls over sensitive employee data.

What would be the most appropriate directive control in this area?

Require a Service Organization Controls (SOC) report from the service provider

Include a data protection clause in the contract with the service provider.

Obtain a nondisclosure agreement from each employee at the service provider who will handle sensitive data.

Encrypt the employees ' data before transmitting it to the service provider

A directive control is a policy, procedure, or guideline that establishes expected behavior to mitigate risks. In the context of outsourcing HR functions, a data protection clause in the contract ensures that the service provider is legally obligated to protect sensitive employee data.

Legal and Regulatory Compliance – It ensures the service provider complies with GDPR, CCPA, ISO 27001, SOC 2, and other data protection laws.

Defines Security Responsibilities – Specifies encryption, access controls, data retention policies, and penalties for non-compliance.

Enforceable Accountability – The contract holds the provider accountable for data breaches or misuse.

Industry Best Practice – Most outsourcing agreements include a Data Processing Agreement (DPA) as part of contractual terms.

A. Require a SOC report – A SOC (Service Organization Control) report assesses the provider’s internal controls, but it does not enforce compliance.

C. Obtain a nondisclosure agreement (NDA) – An NDA is useful, but it only prevents individuals from sharing data; it does not define data security requirements.

D. Encrypt the employees' data before transmitting it – Encryption is a strong preventive control, but it does not provide a directive policy like a contract clause does.

IIA’s International Professional Practices Framework (IPPF) – Standard 2201 – Requires internal auditors to assess contract terms related to risk management.

COSO’s Enterprise Risk Management (ERM) Framework – Recommends contractual agreements for third-party risk mitigation.

ISO 27001 Annex A.15.1.2 – Specifies that security requirements must be addressed in supplier contracts.

Why a Data Protection Clause Is the Most Appropriate Directive Control?Why Not the Other Options?IIA References:✅ Final Answer: B. Include a data protection clause in the contract with the service provider. (Most appropriate directive control).

Which of the following concepts of managerial accounting is focused on achieving a point of low or no inventory?

Theory of constraints.

Just-in-time method.

Activity-based costing.

Break-even analysis

The Just-in-Time (JIT) method is a managerial accounting and inventory management strategy that focuses on reducing or eliminating excess inventory by receiving goods only as needed.

(A) Theory of constraints.

Incorrect: The theory of constraints focuses on identifying and managing bottlenecks in production, not reducing inventory levels.

(B) Just-in-time method. (Correct Answer)

JIT aims to reduce waste, lower storage costs, and improve efficiency by ensuring that materials and products arrive only when needed.

IIA GTAG 3 – Continuous Auditing suggests monitoring inventory controls to align with JIT principles.

(C) Activity-based costing.

Incorrect: Activity-based costing allocates costs to activities based on usage, not inventory reduction.

(D) Break-even analysis.

Incorrect: Break-even analysis calculates the level of sales needed to cover costs but does not focus on inventory management.

IIA Standard 2120 – Risk Management: Encourages auditors to assess cost-management strategies like JIT.

IIA GTAG 3 – Continuous Auditing: Supports real-time monitoring of inventory to minimize excess stock.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (B) Just-in-Time (JIT) method, as it focuses on achieving low or no inventory to optimize efficiency and reduce costs.

Management has decided to change the organizational structure from one that was previously decentralized to one that is now highly centralized. As such: which of the

following would be a characteristic of the now highly centralized organization?

Top management does little monitoring of the decisions made at lower levels.

The decisions made at the lower levels of management are considered very important.

Decisions made at lower levels in the organizational structure are few.

Reliance is placed on top management decision making by few of the organization's departments.

A highly centralized organization is one where decision-making authority is concentrated at the top management level, with lower levels having minimal autonomy. This change means that most critical decisions are made at the corporate level, and lower-level managers have limited decision-making power.

(A) Incorrect – Top management does little monitoring of the decisions made at lower levels.

In a centralized organization, top management monitors and controls most decisions.

This statement applies more to decentralized structures where decision-making is distributed.

(B) Incorrect – The decisions made at the lower levels of management are considered very important.

In a centralized structure, decisions made at lower levels hold less significance since authority is concentrated at the top.

(C) Correct – Decisions made at lower levels in the organizational structure are few.

Centralized structures limit decision-making power at lower levels, keeping control with top executives.

Lower-level managers mostly follow directives from upper management rather than making independent decisions.

(D) Incorrect – Reliance is placed on top management decision-making by few of the organization’s departments.

In a centralized system, most (not just a few) departments rely on top management for decision-making.

IIA’s Global Internal Audit Standards – Organizational Governance and Decision-Making

Explains centralized vs. decentralized structures and their impact on risk management.

COSO’s ERM Framework – Governance and Decision Authority

Discusses the implications of centralization on strategic decision-making.

IIA’s Guide on Corporate Governance and Internal Control Frameworks

Highlights the effect of centralization on accountability, oversight, and risk management.

Analysis of Answer Choices:IIA References and Internal Auditing Standards:

An organization is considering integration of governance, risk., and compliance (GRC) activities into a centralized technology-based resource. In implementing this GRC

resource, which of the following is a key enterprise governance concern that should be fulfilled by the final product?

The board should be fully satisfied that there is an effective system of governance in place through accurate, quality information provided.

Compliance, audit, and risk management can find and seek efficiencies between their functions through integrated information reporting.

Key compliance and risk metrics can be tracked and compared throughout the enterprise, aiding in identifying problem departments.

Data analytics can be utilized for trending of the data to ensure that patterns and ongoing monitoring occurs throughout the organization.

When an organization integrates governance, risk, and compliance (GRC) activities into a centralized technology-based resource, enterprise governance must ensure that the system:

Supports strategic decision-making by the board and senior management.

Provides accurate, reliable, and quality information to demonstrate an effective governance framework.

Aligns with IIA Standard 2110 – Governance, which requires auditors to assess whether the organization’s governance structure supports accountability, transparency, and effective decision-making.

(A) The board should be fully satisfied that there is an effective system of governance in place through accurate, quality information provided. (Correct Answer)

Governance is about ensuring that stakeholders, particularly the board, have confidence in the organization's control environment and decision-making process.

IIA Standard 2110 (Governance) states that internal auditors must evaluate the adequacy and effectiveness of governance structures.

A GRC system should ensure transparency, accountability, and quality reporting to enable strategic governance oversight.

(B) Compliance, audit, and risk management can find and seek efficiencies between their functions through integrated information reporting.

While improving efficiency is a benefit of a GRC system, it is a secondary objective, not a primary enterprise governance concern.

(C) Key compliance and risk metrics can be tracked and compared throughout the enterprise, aiding in identifying problem departments.

Tracking risk metrics is useful but does not directly address governance at the board level, making this answer incomplete.

(D) Data analytics can be utilized for trending of the data to ensure that patterns and ongoing monitoring occurs throughout the organization.

Analytics support monitoring, but the core governance concern is ensuring the board’s confidence in the system.

IIA Standard 2110 – Governance: Internal auditors must assess whether governance processes are effective.

GTAG 1 – Information Technology Risks and Controls: IT governance must provide quality, reliable information for decision-making.

COSO ERM Framework: Emphasizes governance as a key driver of enterprise risk management.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (A) because effective enterprise governance relies on accurate and high-quality information for strategic decision-making.

An organization has an agreement with a third-party vendor to have a fully operational facility, duplicate of the original site and configured to the organization's needs, in order to quickly recover operational capability in the event of a disaster, Which of the following best describes this approach to disaster recovery planning?

Cold recovery plan,

Outsourced recovery plan.

Storage area network recovery plan.

Hot recovery plan

A hot recovery plan (hot site) is a fully operational, duplicate site that is pre-configured and ready for immediate use in case of a disaster. This approach allows an organization to recover critical operations quickly with minimal downtime.

(A) Cold recovery plan.

Incorrect: A cold site is a facility that has infrastructure but no active IT systems or data until set up after a disaster, resulting in longer recovery times.

(B) Outsourced recovery plan.

Incorrect: Outsourcing recovery refers to third-party disaster recovery services, but does not specifically describe a fully operational duplicate site.

(C) Storage area network recovery plan.

Incorrect: A storage area network (SAN) recovery plan focuses on data storage redundancy, not a fully operational duplicate facility.

(D) Hot recovery plan. (Correct Answer)

A hot site is the fastest and most effective disaster recovery solution, ensuring immediate failover with minimal downtime.

IIA GTAG 10 – Business Continuity Management highlights hot sites as the most effective for mission-critical operations.

IIA GTAG 10 – Business Continuity Management: Recommends hot sites for critical recovery scenarios.

IIA Standard 2120 – Risk Management: Emphasizes preparedness for disaster recovery planning.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (D) Hot recovery plan, as it ensures a fully operational backup site for immediate disaster recovery.

According to 11A guidance on it; which of the following statements is true regarding websites used in e-commerce transactions?

HTTP sites provide sufficient security to protect customers' credit card information.

Web servers store credit cardholders' information submitted for payment.

Database servers send cardholders’ information for authorization in clear text.

Payment gatewaysauthorizecredit cardonlinepayments.

E-commerce transactions involve multiple security layers to ensure the protection of customers' sensitive financial information. The correct answer is D, as payment gateways serve as intermediaries that authorize online credit card transactions by securely transmitting the payment details to the bank or card networks for approval. Let’s examine each option carefully:

Option A: HTTP sites provide sufficient security to protect customers' credit card information.

Incorrect. HyperText Transfer Protocol (HTTP) does not provide encryption, meaning that data transmitted over an HTTP connection can be intercepted by malicious actors. Instead, Secure HTTP (HTTPS), which uses Secure Sockets Layer (SSL) or Transport Layer Security (TLS), is required to encrypt the data.

IIA Reference: Internal auditors evaluating e-commerce security should verify that organizations use HTTPS for secure transactions. (IIA GTAG: Information Security Governance)

Option B: Web servers store credit cardholders' information submitted for payment.

Incorrect. While web servers may temporarily process customer data, they should not store sensitive credit card information due to security risks. Instead, organizations follow the Payment Card Industry Data Security Standard (PCI DSS), which mandates secure storage and encryption protocols.

IIA Reference: IIA Standards recommend compliance with PCI DSS to protect sensitive payment information. (IIA Practice Guide: Auditing IT Governance)

Option C: Database servers send cardholders’ information for authorization in clear text.

Incorrect. Transmitting cardholder data in clear text is a severe security vulnerability. Secure encryption protocols such as SSL/TLS or tokenization must be used to protect data in transit.

IIA Reference: Internal auditors should ensure encryption measures are in place for financial transactions. (IIA GTAG: Auditing Cybersecurity Risk)

Option D: Payment gateways authorize credit card online payments.

Correct. Payment gateways act as secure intermediaries between merchants and payment processors, verifying the transaction details before authorization. This ensures a secure transaction by encrypting sensitive data before transmitting it for approval.

IIA Reference: IIA guidance on IT controls emphasizes the importance of secure payment processing through payment gateways. (IIA GTAG: Managing and Auditing IT Vulnerabilities)

Which of the following describes a third-party network that connects an organization specifically with its trading partners?

Value-added network (VAN).

Local area network (LAN).

Metropolitan area network (MAN).

Wide area network (WAN).

A Value-Added Network (VAN) is a third-party network service that securely connects an organization with its trading partners, facilitating secure electronic data interchange (EDI) and business communications.

(A) Value-added network (VAN). (Correct Answer)

A VAN is a private, managed network service that provides secure data transmission between business partners.

It is commonly used for B2B transactions, supply chain management, and EDI.

IIA GTAG 7 – IT Outsourcing recognizes VANs as critical third-party networks for secure business data exchange.

(B) Local area network (LAN).

Incorrect: A LAN connects computers within a limited area (e.g., an office or building), but it is not designed for external trading partner connections.

(C) Metropolitan area network (MAN).

Incorrect: A MAN covers a city or region, but it is not designed for B2B communication.

(D) Wide area network (WAN).

Incorrect: A WAN connects multiple geographic locations, but it is a general networking term, not specific to trading partner communications.

IIA GTAG 7 – IT Outsourcing: Discusses the use of third-party networks like VANs for secure data exchange.

IIA Standard 2110 – Governance: Recommends secure third-party integration for business continuity and security.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (A) Value-Added Network (VAN) because it is specifically designed for secure communication between an organization and its trading partners.

An organization created a formalized plan for a large project. Which of the following should be the first step in the project management plan?

Estimate time required to complete the whole project.

Determine the responses to expected project risks.

Break the project into manageable components.

Identify resources needed to complete the project

The first step in a project management plan is to break the project into manageable components, known as Work Breakdown Structure (WBS). This step ensures clarity, task allocation, and effective tracking.

(A) Estimate time required to complete the whole project.

Incorrect: Time estimation comes after breaking the project into smaller tasks.

(B) Determine the responses to expected project risks.

Incorrect: Risk management is important but is planned after defining project tasks and scope.

(C) Break the project into manageable components. (Correct Answer)

Dividing the project into smaller tasks (WBS) helps in resource allocation, scheduling, and risk assessment.

IIA GTAG 12 – Project Risk Management suggests using WBS to define tasks clearly.

(D) Identify resources needed to complete the project.

Incorrect: Resources can only be allocated effectively after defining project components.

IIA GTAG 12 – Project Risk Management: Recommends Work Breakdown Structure (WBS) as the first step in project planning.

PMBOK (Project Management Body of Knowledge): Defines WBS as the foundation of project planning.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (C) Break the project into manageable components, as this is the first step in structuring and planning a successful project.

An analytical model determined that on Friday and Saturday nights the luxury brands stores should be open for extended hours and with a doubled number of employees

present; while on Mondays and Tuesdays costs can be minimized by reducing the number of employees to a minimum and opening only for evening hours Which of the

following best categorizes the analytical model applied?

Descriptive.

Diagnostic.

Prescriptive.

Prolific.

Descriptive Analytics – Answers "What happened?" by summarizing past data.

Diagnostic Analytics – Answers "Why did it happen?" by identifying causes of trends or issues.

Prescriptive Analytics – Answers "What should we do?" by providing data-driven recommendations and optimal solutions for decision-making.

Prolific Analytics – This is not a recognized category in standard analytics models.

The model makes specific recommendations for store operations (extended hours, staffing adjustments).

It optimizes resource allocation based on demand patterns.

It goes beyond identifying past trends (descriptive) or diagnosing causes (diagnostic) and provides actionable solutions.

A. Descriptive – Would only summarize sales data but not suggest changes.

B. Diagnostic – Would explain why luxury stores see higher traffic on weekends but would not recommend actions.

D. Prolific – Not a standard analytics category.

IIA’s GTAG on Data Analytics – Describes prescriptive analytics as the highest level of business intelligence, driving decision-making.

COSO’s Enterprise Risk Management (ERM) Framework – Encourages data-driven decision-making using prescriptive models.

COBIT 2019 on IT Governance – Recommends leveraging prescriptive analytics for operational efficiency.

Types of Analytical Models in Business Intelligence:Why Prescriptive Analytics is the Best Choice?Why Not the Other Options?IIA References:✅ Final Answer: C. Prescriptive.

Which of the following best describes owner's equity?

Assets minus liabilities.

Total assets.

Total liabilities.

Owners contribution plus drawings.

Owner’s equity represents the residual interest in a company’s assets after deducting liabilities. It is a fundamental concept in financial accounting, reflecting the net worth of a business.

Formula:Owner’s Equity=Assets−Liabilities\text{Owner’s Equity} = \text{Assets} - \text{Liabilities}Owner’s Equity=Assets−Liabilities

Represents the True Value of Ownership – It measures the owner's claim on the business after settling all obligations.

Directly Tied to the Accounting Equation – Assets=Liabilities+Owner’s Equity\text{Assets} = \text{Liabilities} + \text{Owner’s Equity}Assets=Liabilities+Owner’s Equity Rearranging the equation: Owner’s Equity=Assets−Liabilities\text{Owner’s Equity} = \text{Assets} - \text{Liabilities}Owner’s Equity=Assets−Liabilities

Commonly Used in Financial Statements – Found in the Balance Sheet under the "Equity" section.

B. Total assets – Incorrect because assets include both owner-financed and liability-financed resources.

C. Total liabilities – Incorrect because liabilities represent debts owed, not ownership value.

D. Owner’s contribution plus drawings – Incorrect because it only considers investments and withdrawals, not retained earnings or net assets.

IIA’s GTAG on Business Financial Management – Discusses financial statement analysis, including owner’s equity.

COSO’s Internal Control – Integrated Framework – Highlights financial reporting accuracy, including equity calculations.

IFRS & GAAP Accounting Standards – Define owner’s equity as assets minus liabilities in financial reporting.

Why Option A is Correct?Why Not the Other Options?IIA References:

An internal auditor is reviewing key phases of a software development project. Which of the following would; the auditor most likely use to measure the project team's performance related to how project tasks are completed?

A balanced scorecard.

A quality audit

Earned value analysis.

Trend analysis

Earned Value Analysis (EVA) is a project management technique that integrates scope, time, and cost data to measure project performance and progress objectively. EVA allows internal auditors to assess whether a software development project is on track by comparing planned work with completed work and actual costs.

Here’s why EVA is the most appropriate choice:

Evaluates Project Progress and Performance – EVA measures how much work has been completed against the planned schedule and budget, helping auditors analyze project efficiency.

Identifies Deviations – It highlights cost overruns or delays in task completion, which is critical for software development projects.

Uses Key Metrics – EVA includes essential indicators like:

Planned Value (PV) – The budgeted cost of work scheduled.

Earned Value (EV) – The value of actual work performed.

Actual Cost (AC) – The real cost incurred for work completed.

Schedule Variance (SV) and Cost Variance (CV) – Indicators of deviations from planned performance.

Supports Risk-Based Internal Audit Approach – The IIA emphasizes risk-based auditing, and EVA helps auditors assess risks related to project cost overruns, schedule slippage, and performance gaps.

A. A Balanced Scorecard – This measures overall organizational performance across perspectives (financial, customer, internal processes, and learning & growth), but it is not specifically designed for evaluating project task completion.

B. A Quality Audit – This focuses on compliance with quality standards and does not measure project task completion efficiency.

D. Trend Analysis – This evaluates patterns over time but does not provide a structured measurement of project progress in terms of cost, time, and completion percentage.

The IIA’s GTAG (Global Technology Audit Guide) on IT Project Management – Recommends using earned value analysis for project auditing.

IIA’s International Professional Practices Framework (IPPF) – Performance Standard 2120 (Risk Management) – Emphasizes the need for internal auditors to evaluate the effectiveness of project risk management, which EVA supports.

COSO’s Enterprise Risk Management (ERM) Framework – Encourages structured performance measurement techniques like EVA to monitor projects.

Why Not the Other Options?IIA References:Thus, Earned Value Analysis (EVA) is the correct answer because it provides a precise, quantitative way to measure project performance. ✅

Which of the following would an organization execute to effectively mitigate and manage risks created by a crisis or event?

Only preventive measures.

Alternative and reactive measures.

Preventive and alternative measures.

Preventive and reactive measures.

To effectively mitigate and manage risks during a crisis, organizations must implement a combination of preventive and reactive measures:

Preventive measures: These are proactive steps taken before a crisis to reduce the likelihood of occurrence (e.g., risk assessments, internal controls, security protocols).

Reactive measures: These are actions taken after a crisis occurs to minimize damage, restore operations, and recover from the event (e.g., business continuity plans, incident response strategies).

(A) Incorrect – Only preventive measures.

While prevention is essential, not all crises can be avoided. Organizations also need response mechanisms.

(B) Incorrect – Alternative and reactive measures.

Alternative measures (e.g., backup systems) are part of risk management, but without prevention, risks may escalate.

(C) Incorrect – Preventive and alternative measures.

Alternative measures (e.g., backup resources) help maintain operations but do not directly address crisis response.

(D) Correct – Preventive and reactive measures.

Best practice in risk management includes both preventing crises and responding effectively when they occur.

IIA’s Global Internal Audit Standards – Crisis Management and Business Resilience

Emphasizes the need for both prevention and response strategies.

COSO’s ERM Framework – Risk Management in Crisis Situations

Recommends a combination of risk avoidance, mitigation, and crisis response.

ISO 22301 – Business Continuity Management

Highlights the importance of preventive controls and reactive response planning.

Analysis of Answer Choices:IIA References and Internal Auditing Standards:

Which of the following controls would be most efficient to protect business data from corruption and errors?

Controls to ensure data is unable to be accessed without authorization.

Controls to calculate batch totals to identify an error before approval.

Controls to encrypt the data so that corruption is likely ineffective.

Controls to quickly identify malicious intrusion attempts.

To efficiently protect business data from corruption and errors, the best approach is proactive detection through validation controls. Batch total calculations help verify data integrity before approval, ensuring errors are caught early.

(A) Controls to ensure data is unable to be accessed without authorization.

Incorrect: Access controls prevent unauthorized access, but they do not detect or prevent data corruption/errors.

(B) Controls to calculate batch totals to identify an error before approval. (Correct Answer)

Batch control totals ensure that data entries match expected values before processing, helping detect errors before approval.

IIA GTAG 3 – Continuous Auditing recommends automated validation and reconciliation checks for data integrity.

(C) Controls to encrypt the data so that corruption is likely ineffective.

Incorrect: Encryption protects data confidentiality, but it does not prevent or detect errors or corruption.

(D) Controls to quickly identify malicious intrusion attempts.

Incorrect: Intrusion detection systems focus on cybersecurity, not data corruption or errors.

IIA Standard 2120 – Risk Management: Recommends controls for error prevention and early detection.

IIA GTAG 3 – Continuous Auditing: Suggests automated validation processes like batch totals to detect errors before approval.

Analysis of Each Option:IIA References Supporting the Answer:Thus, the correct answer is (B) because batch total calculations effectively detect errors before approval, ensuring data integrity.

Which of the following practices circumvents administrative restrictions on smart devices, thereby increasing data security risks?

Rooting.

Eavesdropping.

Man in the middle.

Session hijacking.

Definition of Rooting:

Rooting (on Android) or Jailbreaking (on iOS) is the process of bypassing manufacturer and administrative security controls on a smart device.

This allows users to gain full control (root access) over the operating system, which can override security restrictions and allow installation of unauthorized applications.

How Rooting Increases Data Security Risks:

Bypassing Security Measures: Rooting removes built-in security protections, making the device more vulnerable to malware, unauthorized access, and data breaches.

Exposure to Malicious Apps: Rooted devices can install third-party applications that are not vetted by official app stores, increasing the risk of data theft, spyware, and ransomware attacks.

Circumventing Enterprise Security Policies: Many organizations use Mobile Device Management (MDM) to enforce security policies, but rooted devices can bypass these controls, exposing corporate data to cyber threats.

Increased Risk of Privilege Escalation Attacks: Attackers can exploit root access to take full control of the device, leading to unauthorized access to sensitive information.

IIA’s Perspective on Cybersecurity Risks:

IIA Standard 2110 – Governance emphasizes the importance of protecting sensitive data and ensuring compliance with IT security policies.

IIA’s GTAG (Global Technology Audit Guide) on Information Security warns against the dangers of rooted or jailbroken devices, as they compromise cybersecurity defenses.

NIST Cybersecurity Framework and ISO 27001 Information Security Standards identify unauthorized modifications to devices as a critical security risk.

Eliminating Incorrect Options:

B. Eavesdropping: This refers to intercepting communications (e.g., listening in on phone calls or network traffic) but does not involve circumventing administrative restrictions.

C. Man-in-the-Middle (MITM) Attack: This is an attack where an attacker intercepts and alters communication between two parties but does not involve rooting a device.

D. Session Hijacking: This attack involves stealing session tokens to impersonate a user but is unrelated to bypassing security controls on devices.

IIA References:

IIA Standard 2110 – Governance and IT Security

IIA GTAG – Information Security Risks

NIST Cybersecurity Framework

ISO 27001 Information Security Standards

Which of the following is the best example of IT governance controls?

Controls that focus on segregation of duties, financial, and change management,

Personnel policies that define and enforce conditions for staff in sensitive IT areas.

Standards that support IT policies by more specifically defining required actions

Controls that focus on data structures and the minimum level of documentation required

IT governance controls ensure that an organization's IT systems align with business objectives, manage risks, and comply with regulatory requirements. These controls cover areas such as security, financial oversight, change management, and operational efficiency.

Let’s analyze each option:

Option A: Controls that focus on segregation of duties, financial, and change management.

Correct.

Segregation of duties (SoD) prevents conflicts of interest and reduces fraud risk.

Financial controls ensure IT expenditures align with budgets and policies.

Change management controls ensure system modifications follow formal approval and testing procedures.

These areas are core components of IT governance, ensuring security, compliance, and efficiency.

IIA Reference: Internal auditors evaluate IT governance using frameworks like COBIT (Control Objectives for Information and Related Technologies) and ISO 27001. (IIA GTAG: Auditing IT Governance)

Option B: Personnel policies that define and enforce conditions for staff in sensitive IT areas.

Incorrect.

While personnel policies support IT security, they do not fully represent IT governance controls. IT governance is broader and includes risk management, compliance, and operational efficiency.

Option C: Standards that support IT policies by more specifically defining required actions.

Incorrect.

Standards are part of IT governance but are not controls themselves. IT governance requires enforcement mechanisms like segregation of duties and change management to ensure compliance.

Option D: Controls that focus on data structures and the minimum level of documentation required.

Incorrect.

While data governance is a subset of IT governance, IT governance includes wider financial, security, and operational controls.

Thus, the verified answer is A. Controls that focus on segregation of duties, financial, and change management.

Which of the following responsibilities would ordinary fall under the help desk function of an organization?

Maintenance service items such as production support.

Management of infrastructure services, including network management.

Physical hosting of mainframes and distributed servers

End-to -end security architecture design.

A help desk function is responsible for providing technical support and maintenance services to end users. This includes troubleshooting issues, production support, and system maintenance rather than managing infrastructure or security architecture.

Let’s analyze each option:

Option A: Maintenance service items such as production support.

Correct. The help desk primarily provides user support, including:

Troubleshooting software and hardware issues

Resolving technical support requests

Assisting users with system access and operational questions

IIA Reference: Internal auditors assess IT service management, including help desk functions, to ensure efficient IT support and incident response. (IIA GTAG: Auditing IT Service Management)

Option B: Management of infrastructure services, including network management.

Incorrect. Infrastructure services (such as network and server management) fall under IT operations or network administration, not the help desk.

Option C: Physical hosting of mainframes and distributed servers

Incorrect. Hosting and maintaining physical servers is the responsibility of data center operations, not the help desk.

Option D: End-to-end security architecture design.

Incorrect. Security architecture design is handled by the IT security team or cybersecurity department, not the help desk.

Thus, the verified answer is A. Maintenance service items such as production support.

Which of the following statements, is true regarding the capital budgeting procedure known as discounted payback period?

It calculates the overall value of a project.

It ignores the time value of money.

It calculates the time a project takes to break even.

It begins at time zero for the project.

The discounted payback period (DPP) is a capital budgeting technique that determines how long it takes for a project’s discounted cash flows to recover its initial investment. Unlike the regular payback period, the DPP accounts for the time value of money by discounting future cash flows.

(A) It calculates the overall value of a project.

Incorrect. The discounted payback period only measures how long it takes to recover the initial investment—it does not determine the overall value of a project. Net Present Value (NPV) and Internal Rate of Return (IRR) are used to evaluate a project's overall value.

(B) It ignores the time value of money.

Incorrect. Unlike the regular payback period, the discounted payback period accounts for the time value of money by discounting future cash flows using a required rate of return.

(C) It calculates the time a project takes to break even. ✅

Correct. The discounted payback period determines how long it takes for the present value of cash inflows to recover the initial investment. It helps assess the risk and liquidity of a project.

IIA GTAG "Auditing Capital Budgeting and Investment Decisions" states that discounted payback is useful for assessing the risk of projects by considering cash flow recovery time.

(D) It begins at time zero for the project.

Incorrect. The calculation starts at time zero (when the investment is made), but the method itself focuses on future discounted cash flows to determine the break-even point.

IIA GTAG – "Auditing Capital Budgeting and Investment Decisions"

COSO ERM Framework – Capital Investment Risk Management

GAAP/IFRS – Discounted Cash Flow Methods

Analysis of Answer Choices:IIA References:Thus, the correct answer is C, as the discounted payback period measures the time needed to break even after adjusting for the time value of money.

An organization has instituted a bring-your-own-device (BYOD) work environment. Which of the following policies best addresses the increased risk to the organization's network incurred by this environment?

Limit the use of the employee devices for personal use to mitigate the risk of exposure to organizational data.

Ensure that relevant access to key applications is strictly controlled through an approval and review process.

Institute detection and authentication controls for all devices used for network connectivity and data storage.

Use management software scan and then prompt parch reminders when devices connect to the network

Understanding BYOD Risks:

A Bring-Your-Own-Device (BYOD) policy allows employees to use personal devices (e.g., laptops, smartphones, tablets) for work.

This increases security risks such as unauthorized access, malware infections, data leakage, and non-compliance with IT security policies.

Why Option C (Detection and Authentication Controls) Is Correct?

Detection and authentication controls ensure that:

Only authorized devices can connect to the organization's network.

User authentication mechanisms (such as multi-factor authentication) verify identities before granting access.

Devices with security vulnerabilities are flagged and restricted.

This aligns with IIA Standard 2110 – Governance, which emphasizes IT security controls for risk mitigation.

ISO 27001 and NIST Cybersecurity Framework also recommend device authentication and monitoring for secure network access.

Why Other Options Are Incorrect?

Option A (Limit personal use of employee devices):

Limiting personal use does not fully address network security risks; malware can still infect devices.

Option B (Control access through approvals and reviews):

While access control is important, it does not mitigate the broader risks of compromised devices connecting to the network.

Option D (Software scans and patch reminders):

Patching is important, but it does not prevent unauthorized access or ensure authentication for devices.

Implementing device detection and authentication controls is the most effective way to mitigate security risks in a BYOD environment.

IIA Standard 2110 and ISO 27001 emphasize strong network security measures.

Final Justification:IIA References:

IPPF Standard 2110 – Governance (IT Risk Management & BYOD Security)

ISO 27001 – Information Security Management

NIST Cybersecurity Framework – Access Control & Authentication

Which of the following network types should an organization choose if it wants to allow access only to its own personnel?

An extranet

A local area network

An Intranet

The internet

An Intranet is a private network that is accessible only to an organization’s personnel. It is used for internal communication, data sharing, and collaboration while ensuring security and restricted access.

Let’s analyze each option:

Option A: An extranet

Incorrect. An extranet extends an organization’s internal network to external parties such as vendors, suppliers, or business partners. Since the organization wants to allow access only to its personnel, an extranet is not the right choice.

Option B: A local area network (LAN)

Incorrect. While a LAN is a network within a limited geographic area (such as an office), it does not necessarily restrict access only to personnel. Additionally, an intranet operates over a LAN but includes access controls and authentication mechanisms.

Option C: An Intranet

Correct. An intranet is specifically designed for internal use, allowing employees to securely share documents, collaborate, and access internal resources. Organizations can implement access control mechanisms to restrict access to authorized personnel only.

IIA Reference: Internal auditors assess IT security to ensure that internal networks (such as intranets) have appropriate access restrictions to protect sensitive data. (IIA GTAG: Auditing IT Networks)

Option D: The internet

Incorrect. The internet is a public network that does not restrict access. Using the internet for internal communication would expose sensitive data to external threats.

Thus, the verified answer is C. An Intranet.

Which of the following situations best applies to an organisation that uses a project, rather than a process, to accomplish its business activities?

Clothing company designs, makes, and sells a new item.

A commercial construction company is hired to build a warehouse.

A city department sets up a new firefighter training program.

A manufacturing organization acquires component parts from a contracted vendor

A project is a temporary initiative with a defined start and end date, specific objectives, and unique deliverables. Unlike ongoing business processes, projects have distinct goals, require coordination across various resources, and are not repeated continuously.

Let’s analyze each option:

Option A: A clothing company designs, makes, and sells a new item.

Incorrect.

While designing a new clothing item could be a project, the production and sale of the item are ongoing processes, not a one-time project.

Option B: A commercial construction company is hired to build a warehouse.

Correct.

Construction projects are classic examples of project-based work because:

They have a defined beginning and end.

They involve unique deliverables (a specific warehouse).

They require temporary coordination of resources.

IIA Reference: Internal auditors assess project management frameworks to ensure compliance with organizational and financial controls. (IIA Practice Guide: Auditing Project Management)

Option C: A city department sets up a new firefighter training program.

Incorrect.

If the training program is a one-time initiative, it could be considered a project. However, if the program is recurring (e.g., new firefighter training every year), it would be a process, not a project.

Option D: A manufacturing organization acquires component parts from a contracted vendor.

Incorrect.

Procurement of component parts is a continuous operational process, not a project.

Thus, the verified answer is B. A commercial construction company is hired to build a warehouse.

An organization's account for office supplies on hand had a balance of $9,000 at the end of year one. During year two. The organization recorded an expense of $45,000 for purchasing office supplies. At the end of year two. a physical count determined that the organization has $11 ,500 in office supplies on hand. Based on this Information, what would he recorded in the adjusting entry an the end of year two?

A debit to office supplies on hand for S2.500

A debit to office supplies on hand for $11.500

A debit to office supplies on hand for $20,500

A debit to office supplies on hand for $42,500

Understanding the Accounting for Office Supplies:

The organization maintains an account for office supplies on hand, which represents unused office supplies at any given time.

The expense recorded during the year represents the cost of office supplies purchased.

At year-end, the adjusting entry is made to reflect the actual amount of supplies on hand and adjust the supplies expense accordingly.

Formula to Determine the Supplies Used:

Supplies Used=Beginning Balance+Purchases−Ending Balance\text{Supplies Used} = \text{Beginning Balance} + \text{Purchases} - \text{Ending Balance}Supplies Used=Beginning Balance+Purchases−Ending Balance

Plugging in the given values: